Berkshire Hathaway vs. KKR

Berkshire Hathaway vs. KKR

The key differences between value investing and private equity

Among a list of unconventional and marvelous ways of approaching investing and conglomerate management, Berkshire Hathaway is well known for thinking and acting long term. Berkshire has more than 60 wholly owned subsidiaries and a long list of equity ownership in publicly traded companies. Among some of the more famous companies that Berkshire still holds today, Berkshare bought See’s Candies in 1972, GEICO in 1976 (though Warren bought his first shares in GEICO back in 1951 when he was still a graduate student in Columbia), and Dairy Queen in 1997. Remarkably, on the easily traded stock market, Berkshare has not sold a single share after it first bought shares in Coca-Cola since 1988 or American Express since 1994 (think for a second how someone on Twitter brags about being a long term holder after 2 years).

Kolberg Kravis Roberts (“KKR”) is often regarded as the pioneer of the modern private equity industry. Founded in 1976, KKR orchestrated some of the largest leveraged buyouts of their time and has since grown to be a diversified alternative asset manager with approximately USD 250billion of AUM. In private equity, a manager (in industry lingo “General Partners” or “GPs”) pool together money from its investors (“Limited Partners” or “LPs”) and invest in companies, hold them for several years and sell the companies in the hope to generate investment returns.

Both Berkshire and KKR have created immense wealth for itself over the past decades. Though their methods and corporate structures differ, on the fundamental level they involves buying and selling stakes in companies. On the surface, both involves some form of fundamental analysis looking at the soundness of the industry, competitive dynamics, business model and management team. But if we peel the onion, at its core the differences can be stark.

After working as an investment professional in a private equity fund for the past 5 years, while practicing Buffett-style value investing for my own stock portfolio for the past 3 years, it always bothers me how different both investment approaches are (and in a subtle and deep-seated way). This article is intended to pen down my thoughts as I am fortunate to have direct experiences on both sides and also find myself always trying to answer this question to people.

1. Let’s Get Married! (p.s. for only 5 years)

Warren Buffett has always said that his preferred holding period for an investment is forever. Though I suspect even Francis Gerety herself didn’t mean it literally when she created the slogan ‘A Diamond is forever’ for DeBeers, I doubt Buffett meant it literally as well (but 50 years of holding See’s Candies surely feels and looks like forever in Wall Street context). To me, the key word in that quote is ‘preferred’, not ‘forever’, as it speaks to the intention rather than the outcome (we will come to that later, as well as more exploration into the analogies between investment and marriage).

On the other hand, private equity funds have a fund life, which is typically 10 years (with up to 2-year extension). The first 5 years, called the investment period, is when the fund manager sources for deals and calls on capital from LPs once a deal is found. The next 5 years will be the period where the fund manager tries to sell its companies in the portfolio. This means that the theoretical maximum period a PE investor can hold an investment is 12 years. In reality, the average holding period ranges from 3 to 6 years. A key observation over the years is that performance of a portfolio company typically inversely correlates with the holding period after the first 3-4 years (i.e., fund managers prefer a quick flip and get a high IRR return, while poor performing companies get ‘stuck’ in the portfolio).

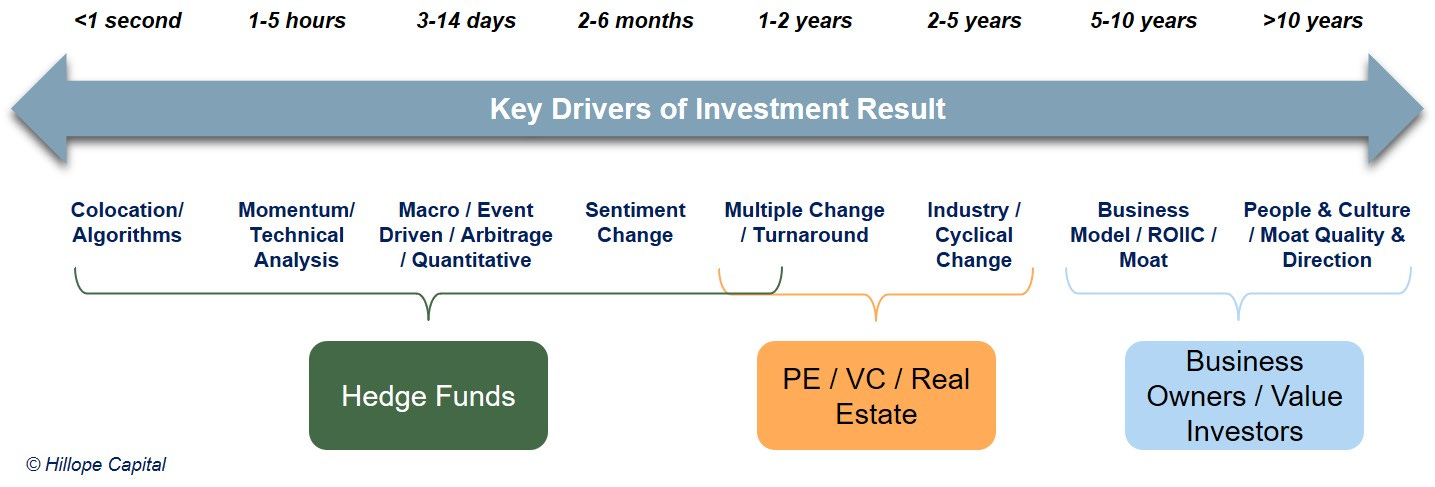

In today’s world of instant gratification and constant impulse to act, many investors would regard a 3 to 7 years holding period as a long enough period to be branded as ‘patient’ capital and true long-term investor. However, the fact of the matter is that the duration in investment holdings, like many things in life, is a relative concept. Take a look at the chart below and you will notice at every timescale, from milliseconds to decades, there are no shortage of people employing various strategies trying to beat the market. 1 minute will look like an eternity to the high-frequency traders, while 1 quarter is imcomprehensible to the business owner/value investor.

This then begs the question - what exactly is the difference between a 3 to 7 year holding period vs. a preferred forever holding period. As it turns out, I think the difference is immense (try asking the same question to your girlfriend or spouse and her reaction should give you a hint). At the core is the difference in incentive-driven mindset, which drives differences in decision-making and behavioural changes which trickles down the organisation from the top.

Since private equity managers already know they are going to exit or sell the company in the next 3-5 years even before they invest in the company, all they are thinking will be how to maximise the exit value. In a typical private equity deal, be it minority growth capital, MBOs or LBOs, the key drivers of exit valuation are profitability (typically EBITDA or NPAT), exit multiple (EV/EBITDA, P/E or P/B) and cash generation. This is why PE fund managers love to pile debt on a company from the get-go (in the fancy name of “balance sheet optimisation”), and then dividend the money out to offset some of the initial purchase considerations (doesn’t it sound similar to the popular saying “borrow your watch to tell you the time” in consulting).

If you know your are bidding farewell to the portfolio company and most likely won’t see each other for the rest of your life, and being in a position of control, what would most people do? Well, the fund manager will likely ‘dress up’ the company in preparation of an exit, paint a fancy growth story, cut costs where possible to increase earnings, stop investing in capex if that ROI only comes in much later and the spending benefits the next buyer instead (and at the detriment of the long term competitive advantage of the company, argh, this one really angers me). In short, fund managers will try all means to decorate the company to ‘juice up’ the returns. The only self-imposed governance mechanism will be the fund’s reputation since they need to keep finding the next ‘target’ and raise a new fund. When the operating timeframe and mindset is only 3 to 6 years, it is sometimes disheartening but not uncommon to see companies being tossed around between private equity funds.

On the other hand, you may observe that some value investor funds also sell their holdings within a few years and may well be less than a typical holding period of a PE fund. Before you accuse me of any hypocrisy, the key difference here is the intention. Businesses are incredibly fragile beings and they have to keep fending off the competition, innovate and adapt in order to survive the Darwinian selection. The fact is the hit rate for finding great companies well-deserving of the “forever-holding” bucket is extremely low (well, Nicholas Sleep found three and decided to close his fund and advised his LPs to put the money in the three themselves). True value investors sell for 3 reasons: i) underlying fundamentals and thesis for the business have changed; ii) we made a mistake; iii) we found something much better. All these are valid reasons to sell. Divorce rates are high, yet most loving couples hope to wed forever. This brings back to my earlier point - value investors prefer forever while seeking true love, PE investors want a bigger piece of the pie in a fling.

Given the above, you may wonder, what then does any company still want to invite such a “barbarians at the gate”? Well, I don’t think there is a simple answer and each company’s situation is different. Also, the above is not representative of all PE deals, a few do try to be a good partner, bring real value add and leave the management team to work their magic. Suffice to say, there are no short of companies looking for private equity money, and also no short of capital chasing too few deals (turn around to take a look at the VC space now and you will get shocked).

2. It’s All About the Fundamentals!

In my work as a private equity investor, the valuation metrics that we use and talk about almost universally are P/E and EV/EBITDA (and sometimes P/B especially for financial service firms). In PE’s fundamental analysis, we are trained to think that a low P/E or EV/EBITDA is cheap (and vice versa). So how low is considered cheap? An interesting observation is that most PE investors seem to have a mental scale in their heads about the kind of multiples that one industry should have vs. others. E.g., in the current environment contract manufacturers or automotive industry should be given 5-6x EV/EBITDA while healthcare or semicon industries will garner low-mid teens EV/EBITDA (it doesn’t help that PE investors often reference the comparables in the often mispriced public markets as the benchmark, as well as what others have paid in the past).

With such an anchor bias, then an analysis of how cheap a company is will be relative to a broad stroke and arbitrary valuation multiples (without much well-deserved considerations of the individual merits of a company). There is almost no mention (at most just an occasional whisper) of intrinsic value, return on equity (ROE), return on capital employed (ROCE), etc. I found this perplexing. How is it possible that a company with a wide moat and unique business model (e.g., Costco) be valued at roughly the same range of multiples as another more inferior company in their respective industry (e.g., Sainsbury’s). The fact is that PE’s fundamental analysis often do not go deep enough to truly understand the business model and drivers, moat and direction of moat, management team and culture, all of which are key determinants of long term value creation. Of course, if you are just holding the investment for 3-5 years, you may not be worse off ignoring these drivers (back to the above time horizon point again, duh!). At its core, a value investor and a PE investor views the fundamentals of a business with a different lens and a different focal point.

3. Swing, You Bum!

“The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, ‘Swing, you bum!,’ ignore them.” - Warren Buffett

Buffett has often compared investing to baseball, and that the key is to wait patiently for the fat pitch. It is no wonder why Berkshire has in recent years been sitting on higher and higher cashpile, which is a clear indication of them not finding the opportunity to swing (though their size limits their investable universe and hence it’s harder for Berkshire to find the right opportunity than an average size fund). There is another subtlety to sitting on a cash pile, which highlights the key differences between Berkshire-style investing vs. KKR-style investing.

Unlike in Berkshire, which is structured in a way to not succumb to institutional imperatives (more about this at the end) and focuses on long-term compounding of a portfolio’s intrinsic value, in private equity once a fund closes the clock starts ticking as the investment period is only 5 years. In a typical PE fund there will be 10-15 portfolio companies, which means in an average year a PE fund has to do 2-3 deals. One of the reasons why LPs put their money with a PE fund is they want the fund manager to find good (and preferably proprietary) deals. If after a couple of years a PE fund can’t deploy the capital that the LPs have committed to them, then the LPs will question the deal-making capability of the GPs and whether fund size is right. It is hard to resist the temptation to swing when everybody else are having a good time swinging and laughing at your inaction. Unless you are deaf, it is almost impossible to ignore when the person yelling at you to swing is the person giving you the money to invest in the first place. Worse still, the KPIs of many PE investment professionals are often judged by how many deals he/she did for the year.

As with the entire alternative asset management industry, even though the PE industry is considered ‘long term’ capital, the temptation to deploy capital to the detriment of performance is pervasive and strong. This has all to do with the fee structure and incentive mechanism which we come to below.

4. Fee Structure Creates the Wrong Incentive

“Job one, two and three for your manager is investment performance, not asset gathering. Few practice this approach … Common sense and simple maths dictate that it will be opportune if growth can be channeled to coincide with depressed prices, and not market tops. We must aim for this standard, even though it is contrary to common practice in the industry. Had we adopted the industry standard open house approach the Partnership would be approximately three times its current size, but the results worse, and the quality of Partners meaningfully impaired.” - Nomal Investment Partnership Letters Jun 2004

Nicholas Sleep’s Nomad Investment Partnership closed in 2014 after a 12-year annualzied return of 20.8% (14.3% outperformance over MSCI World Index over the same period!). Throughout their time managing Nomad, they have mostly closed their fund to new subscriptions because they valued performance higher than asset accumulation. One of the key reasons why they shut their funds after 12 years and returned money to their LPs is because they find it increasingly hard to uncover great investment targets in a frothy external environment.

When is the last time we heard any PE funds closed because their results are excellent but just can’t find good deals. None that I know of. Instead, while the music is playing, most of them will rush to raise a new and bigger fund, touting the success of past returns and how they beat the competitor PE funds (even though quite a number of their after-fee returns struggled to keep up with a passively invested S&P 500 index fund).

The industry norm in the alternative asset management industry is 2/20 (two-twenty), i.e., 2% management fee on AUM and 20% performance fee (triggers only if a minimum 8% hurdle rate is met). The 2% management fee is a guaranteed annual payment regardless of performance, and it is justified by GPs to pay for all the salaries and bonuses, office rentals, fancy research tools, operating expenses (Business Class & 5-star Hotels anyone?), etc. When you have something so sweet in life that’s guaranteed, it is little wonder that PE fund managers will prioritize raising the next fund (and filling up the AUM on the brink of gluttony) over performance of the fund. The implications here are huge. If a fund did well for the first 50% of AUM committed and returned a good amount of money to LPs already, then the GPs is more likely to opt for sub-optimal but safer bets (note that safer is subjective) to ‘balance’ the portfolio, since they need to get to 75% of the committed capital deployed before they can go market and raise the next fund. Also, after the first 5-year investment period, the 2% management fee is paid on invested capital, and hence you can imagine during the last 3 months before the 5th anniversary, GPs will rush to deploy since they know they will earn a management fee on that capital as well. The list goes on.

In the actual operation of a PE fund, you will be surprised how much of the $100 of committed capital actually goes to investing in the companies that actually generate returns. For a typical $100m PE fund, only an estimated $70-75m goes into doing the real work, while $20-25m are expenses over the life time of the fund. Fund expenses (fund admin, audit, legal & compliance), deal-transaction expenses (DD costs, expert networks), and other one-time fees all combine to result in an average differential between the gross return (how much money got returned from money that went into the portfolio companies) and the net return (how much money got returned to LPs from committed capital) to be 7% in IRR and 1.0x in MoM. Next time you see any fund touting the alignment of interests with a 2/20 fee rule, think again….

5. Folly of the Institutional Imperatives

“My most surprising discovery: the overwhelming importance in business of an unseen force that we might call 'the institutional imperative.' In business school, I was given no hint of the imperative's existence and I did not intuitively understand it when I entered the business world. I thought then that decent, intelligent, and experienced managers would automatically make rational business decisions. But I learned over time that isn't so. Instead, rationality frequently wilts when the institutional imperative comes into play.

For example: (1) As if governed by Newton's First Law of Motion, an institution will resist any change in its current direction; (2) Just as work expands to fill available time, corporate projects or acquisitions will materialize to soak up available funds; (3) Any business craving of the leader, however foolish, will be quickly supported by detailed rate-of-return and strategic studies prepared by his troops; and (4) The behavior of peer companies, whether they are expanding, acquiring, setting executive compensation or whatever, will be mindlessly imitated.” - 1989 Berkshire Hathaway Chairman’s Letter

It is one thing to have open mind and always learn the best from what others are doing, it is quite another to become irrational and blindly follow. Corporate world is not short of these follies as observed by Buffett, and which the fund management industry is not insulated from this unseen force. When you see other PE/VC funds pouncing on certain hot sectors, chasing a deal by paying up, and over-leveraging a business, the FOMO nature of the human psychology will kick in.

A certain sector is deemed more favourable with ‘good exit potential’ if there are many prior transactions involving PE funds. PE funds beefing up their portfolio management team and other esoteric specialists in a bid to differentiate themselves from the pack and add more conviction to the LPs that they can ‘value add’ to the companies. Sometimes when a portfolio company performs so well after 3-4 years and is in an ever stronger position to grow and compound capital for longer priod of time, the managers made the decision to sell. You may think most of these “forced-selling” is because the fund life is up, but in fact, from my observation, this is rarely the case. In the Peter Lynch lingo, fund managers often cut the flowers (and water the weeds as well) mainly because they want to show LPs a realized good return (along with a subtle message: please prepare money for our upcoming fund raise), or some buyer came along and offered a high price, or some belief that it’s better to exit now before the macro environment turns sour. Of course, the LPs will pat the back of the fund managers who got them a 5x return, totally oblivious to the true costs of forgoing a 10x or higher return.

And the list goes on.

P.S. Time is the most precious non renewable resource and I thank you for reading up to this point. If you like what I write, leave a comment, subscribe or share it.