AK Medical/爱康医疗 (HK: 1789)

A Leading Orthopaedic Implants Business in China

Before I start my analysis of the company, I want to pen down the special connections I have with this company. I first came across AK Medical in late 2018. Back then, my investment philosophy that I have today wasn’t fully formed yet and I didn’t understand the significance of long-term compounding in quality companies. I was attracted to this stock due to its high growth and margins, and the fact that I was familiar with the industry because one of the first few consulting cases I did as a strategy consultant was in the joint replacement market (this sure reminds me of the famous quote from Steve Jobs’s Stanford Commencement Speech about connecting the dots looking backwards only).

I read the Prospectus, annual reports and public releases. I thought it was a great company with a huge growth potential but then I did nothing. At that time, it was trading at ~ 20-25x for LTM EV/EBITDA and ~30x for P/E, which I thought was too expensive. I was ignorant about how to estimate a company’s true intrinsic value and thinking more deeply about a company’s moat and future cashflow. More importantly, I was stuck with the simple mindset of equating ‘cheapness’ to static valuation multiples both from reading about ‘deep value-investing’ and Ben Graham’s work, but perhaps more deadly from my years of professional work as a private equity investor (I shall write more about the differences being a PE investing vs. value investing in future posts when I have time).

I thought I will keep AK in my watchlist and buy only after it dips, thinking that I was being ‘discipline’ and applying the principle of ‘margin of safety’. Instead, I watched the price went stratospheric from HK$4-5 in mid-2019 to a peak of HK$27 in July 2020 – a 5x increase in about a year! I was cursing myself of not buying the stock with the all-so-common hindsight bias, and all the while trying to stay discipline and not FOMO into it (would you buy a property after its seller raises price by 30%?). At some point I gave it up and stop closely following the price to prevent further emotional stress. Then all out of the blue came the ‘Volume-based Procurement’ policy hammer which knocked the price all the way down from HK$27 to ~HK$9-10 in Mar 2021. After all the emotional roller-coaster, this is the buying opportunity I was waiting for. I did my research (more on it below) and bought the stock in a series of purchases at around HK$9-11.

As of Jun 2021, AK Medical became the largest holdings in my portfolio and I feel really good about it (though time will tell whether my wallet will end up reciprocating my feeling). In the Chinese language there is a term called “缘分”, which loosely translated means fate or destiny. I definitely felt this special connection, or fate, with AK Medical. Ok, enough sentimental talks, now back to the main analysis….

Business Introduction: Founded in 2003, AK Medical is a leading orthopaedic implants company in China focusing on R&D, manufacturing and sales of its own branded hip, knee and spine implants. It has the largest market share in joint replacement implants in terms of volume among all domestic and foreign brands. AK was the first medical device company in China to commercialise the application of 3D printing technology to orthopaedic implants, and has launched the first NMPA-approved 3D-printed acetabula cups in 2015. The company has grown at a 38% CAGR in sales and 35% CAGR in net income from 2014 to 2020, with average ROCE of ~70% and ROE of ~35% over past 6 years. It mainly sells its products to a network of distributors across the country who will then sell it to hospitals.

Summary of my investment thesis (TLDR version):

Large and predictably fast-growing market driven by macro-economic factors – aging population, rising prevalence and incidence rate of joint disorders, greater penetration rate of joint surgeries and rising expenditure on medical devices

Import substitution trend will steadily lead to dominance of domestic brands

Multi-disciplinary nature and manufacturing prowess of Chinese companies create an inherent moat for the medical device

Clear leader in 3D-printed orthopaedic implants demonstrates strength of R&D capability and barriers to entry

Best positioned to benefit from (or least affected by) the Volume-based Procurement policies to be implemented

Owner-operator with founder trained as an orthopaedic doctor

Demonstration of M&A capability and global ambition

Key Potential Risks and Concerns:

The single largest risk happening now is regulatory. This itself warrant a full 2-3 posts of discussion but I won’t go into detail here. In short, the implementation of Volume-based Procurement policy (Jicai or 集采) has far-reaching implications on a whole bunch of factors - pricing & margins, surgery volume and demand, changes to import substitution trend, sales channel and marketing, etc.

Product quality issue leading to recalls or medical adverse events

Channel stuffing leading to overestimated sales and profit

1. 骨科的风口,连大象也能飞起来

Lei Jun of Xiaomi coined the phrase ‘站在风口上,猪都能飞起来!’ to describe how an entrepreneur should choose industries with such strong macro-economic tailwinds that practically anyone can make it successful. To me, the orthopaedic market in China can lift up an elephant, and the ‘风口’ can be sustained for at least the next 5-10 years, due to the following key drivers:

Rapidly aging population - China’s aging population issue has been widely publicised and considered the most staggering pace of aging any country has ever seen. The number of 65+ years old has increased from 100mn (7.7% of population) in 2005 to 175mn in 2020 (12.5% of population), and is projected to grow to 260mn by 2030 (17% of population), and 360mn in 2050 (26% of population). That’s more than the total population of U.S. today! Orthopaedic implants, especially hip and knee implants, are mainly used to treat osteoarthritis (OA) and rheumatoid arthritis (RA), both of which are common chronic illnesses that are strongly coorelated with old age.

Many scientific articles have been published on the prevalence and incidence rate of osteoarthritis globally. In China, incidence rate of osteoarthritis in people aged 50 and above is almost 50%, and that for 60+ is ~62%. Key points to note here are that both prevalence and incidence rates are increasing over time, particularly in developing countries, as people generally live longer and getting richer with more sedentary lifestyle (too much sports or running can also lead to joint problems). Some studies have shown that the prevalence rate in Asian countries are even higher than in Europe or USA.

Despite no less incidence rate in China vs. the rest of the world, the penetration rate of joint replacement surgeries are way lower in China compared to the rest of the developed countries. As an example, penetration rate of joint replacement surgeries per 60+ population are 0.4% in China, vs. ~2.5% in US and ~4% in Germany. This is not due to the surgery being difficult to perform or efficacy not proven. In fact, arthroplasty has one of the highest success rates of all surgeries. Two main reasons for the discrepancy are supply side issue with a lack of qualified orthopaedic surgeons in China and demand side issue where patients have less access to medical care, less willing to undergo surgery (especially for older people), and high cost. If we assume all else equal but just adjusting the penetration rate of China from 0.4% to 1.5% (half of the global average of 3%), that in itself implies a 4x growth in the 2020 surgery number, or over a 10-year period CAGR of 15%!

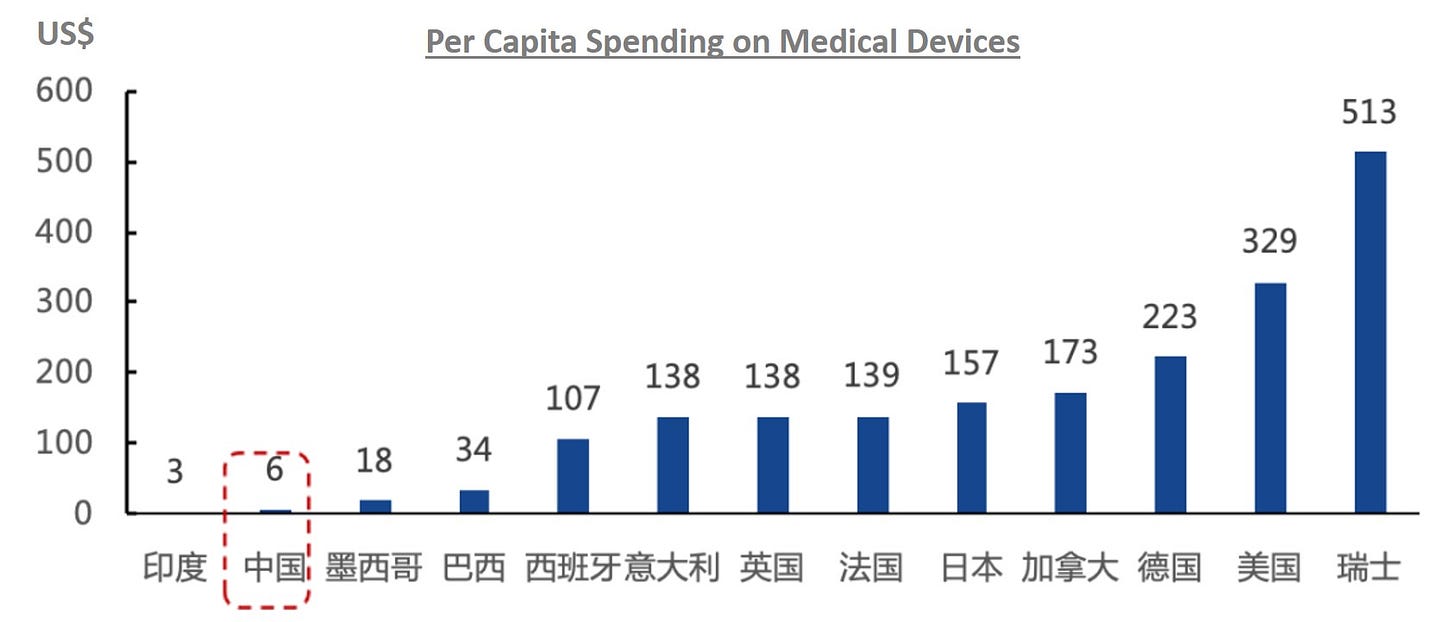

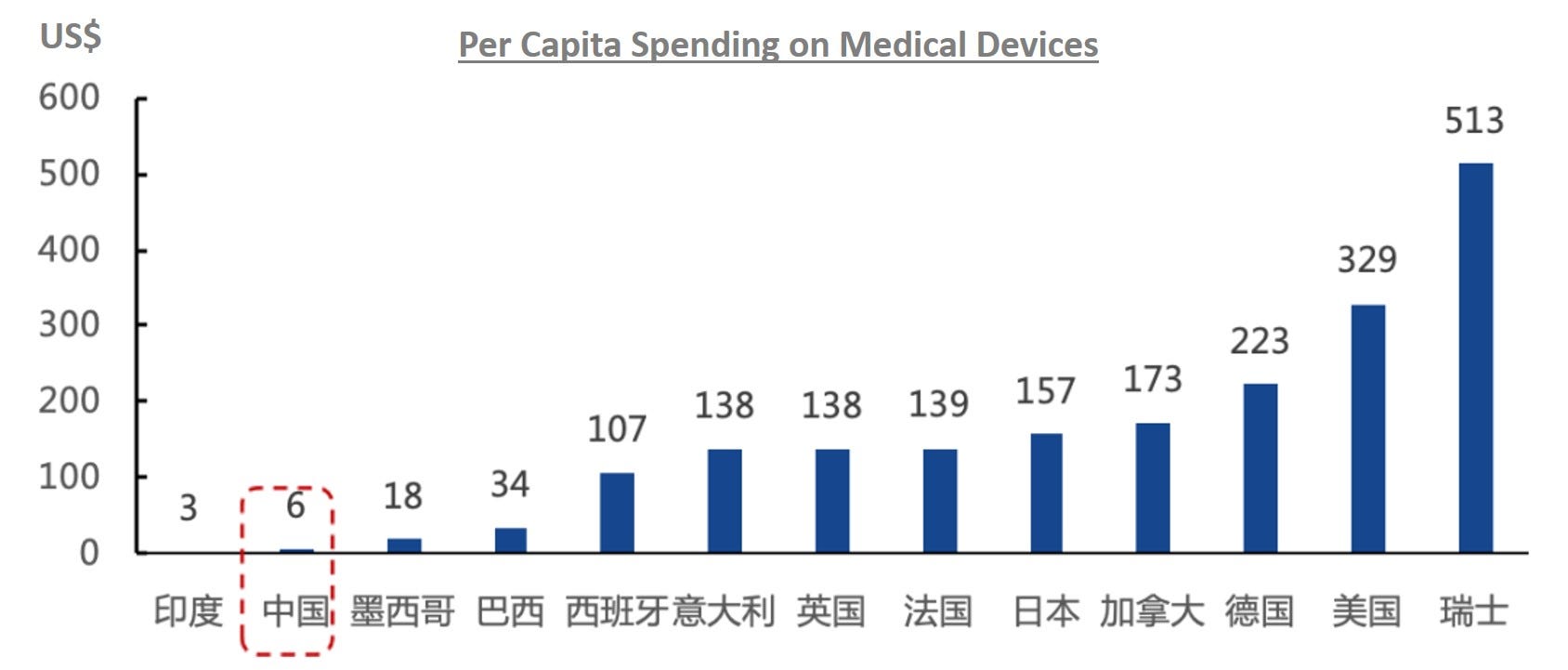

Globally, the ratio of government healthcare spending on medical devices vs. pharmaceuticals is on average 35-40% in developed countries such as USA and Europe but only 15% in China. This was due to China’s unique healthcare developmental path which puts more focus into pharmaceuticals but this gap is expected to close as China focuses more resources on medical devices and high-value consumables. We can see in the chart below the staggering gap in per capita spending on medical devices between the countries, in which China is definitely being downplayed relative to its GDP per capita.

Another interesting fact: If we delve into the three sub-segments of orthopaedics, globally joint reconstruction is the largest with ~37% market share, followed by spine and trauma. However, in China joint replacement lags behind the other two segments.

I think any one of the above factors in itself will drive the growth of joint replacement implants, just like how a mature orthopaedic device market like the US have grown steadily over the recent years and supported the emergence of giant medtech companies like Stryker, Zimmer and DePuy Synthes (though a significant part of their growth story is also due to well-executed acquisitions). But it is the combination of all these three drivers acting in the same direction and reinforcing each other that will really drive the growth in China for a long time to come (such a share gain in a growing pie effect is why I think an elephant will fly!).

2. 进口替代,趋势无法挡

Import substitution is one of the ongoing megatrends being played out across various sectors in the Chinese market, be it in electric vehicle, semiconductors, aerospace engineering, telecom & 5G, etc. The core of the current import substitution megatrend is technology innovation and moving up the value chain, which China views as one of the core strategies to modernize and grow its economy in the future decades. China wants to transition from being the ‘factory of the world’ to being the ‘factory + brain of the world’ - a technology powerhouse to compete with the developed world.

Within each industry there are certain sub-sectors where import subsitution has been completed while others are still in early stages - e.g., in eletric vehicle sector, China has already caught up and became a real competitor in EVs, but still lacks in core technology such as semiconductor chips, AI, Lidar, etc. Having said that, China is catching up very fast, particularly with the US-Sino trade war heating up in the background and has propelled greater urgency within the Chinese government.

In my opinion, this megatrend has three fundamental supporting drivers which will help propel domestic companies to compete and dominate the imported brands in the medical device industry:

Favoritism policy by the government, which is something that the government is not shy of making it clear to market players. This manifests itself in various ways - e.g., in terms of % reimbursement from the public health system (see below), easier and quicker approval process for innovative drugs and devices (a.k.a. “green channels”), etc. There are numerous policy and clear signal from the highest echelon in the CCP that they view this as a priority, and I believe this type of favoritism policies will not change for the foreseeable future.

Over the past 10-15 years, Chinese companies have generally shifted their mindset and understood the importance of R&D, innovation and IPs. From the government’s top-down regulatory and financial support, to a highly educated population breeding many visionary enterpreneurs, to capital market’s influx of money, all these have led to an environment of rapid innovation and increasing quality of products and services at a much lower cost (and Chinese have started to gradually move from improvising copycats to true innovators in some sectors). This serves as a core foundation on which the value and quality of domestic products can match imported brands.

On the demand side, I think more Chinese consumers have become educated and well-travelled, and hence more discerning in terms of product selection rather than having blind faiths in ‘imported products are better’ kind of mindset. This is particularly true for the younger generations who increasingly want to embrace and support domestic brands, partly due to nationalistic sentiments and narrowing gap between product qualities between domestic and imported products.

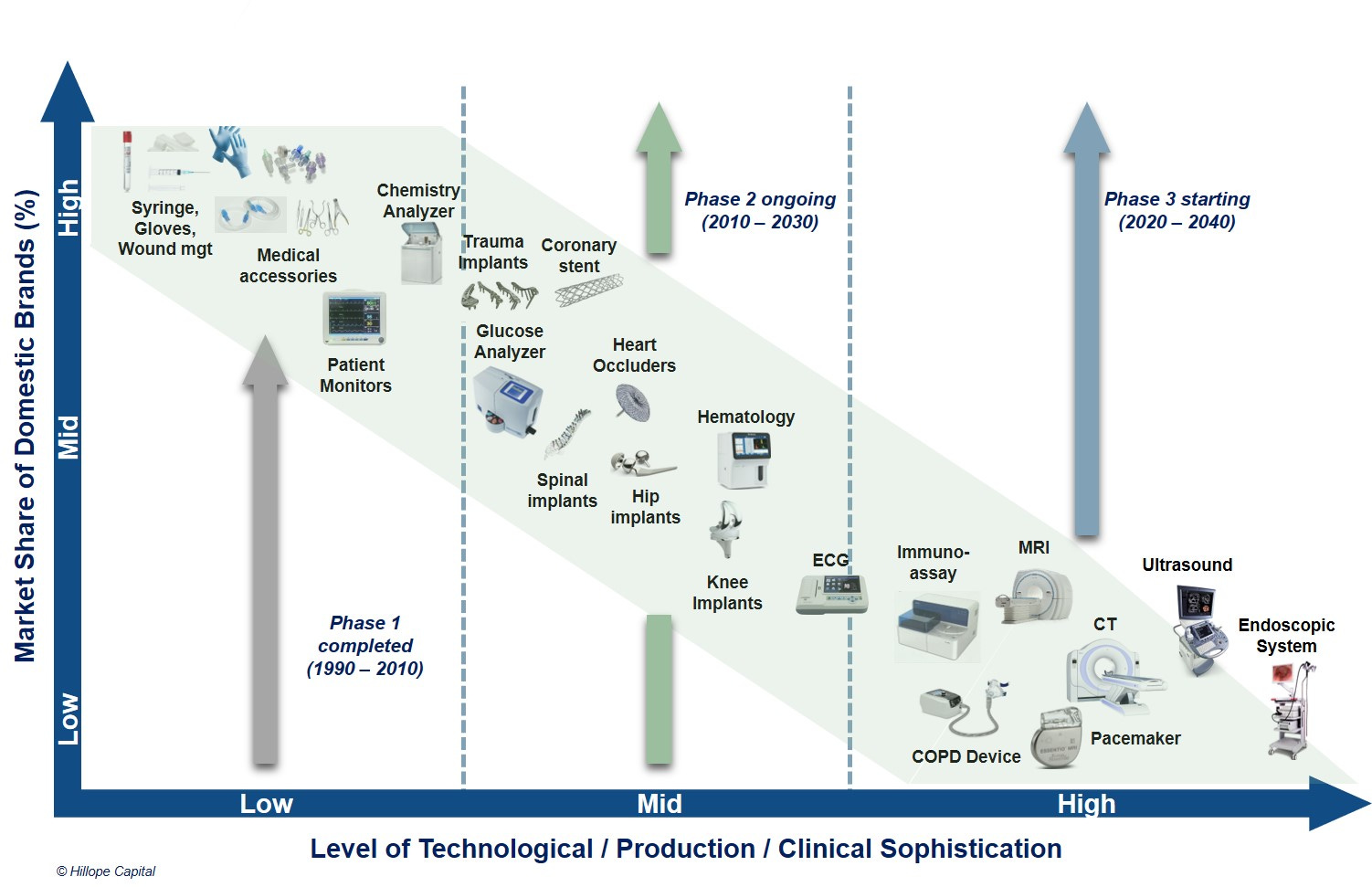

All the above serve as strong driving forces for domestic brands to gradually take market share from imported brands, which are being played out across various sectors. In the medical device space, if we largely divide the sector into three levels of clinical or technological sophistication (see slide below), the low-value medical consumables and equipment have mostly achieved import substitution over the past 20-30 years, while the middle segment is currently undergoing a rapid trend of import substitution, and the high-value segment (largely consist of large medical devices such as CT and MRI scanners) is now just starting. A yearly time series animation of the slide below will see an original flat horizontal line at the bottom gradually rise to become a nice downward slope. I believe such an animated chart is being played out in various stages of development across multiple difference industries in China.

It’s worth talking about an example in the coronary heart stent market to illustrate the staggering pace of this trend. Prior to 2005, heart stents are 95% dominated by foreign brands such as J&J, Medtronic and Boston Scientific, but after domestic Medtech pioneers Microport and Lepu launched their own stent products back in 2004 and 2005, it took merely 4 years for domestic products to reach 70% market share! Today, it hovers around 80-85%. It’s a fascinating case study on why such a dramatic switching can occur on a Class III medical device, but I will leave it for another day.

3. 药品与器械的差异造就了护城河

To analyze the Medtech industry, it serves up great insights to analyze the parallels between Medtech and pharma industries. Two interesting observations:

The global top Medtech companies have stayed more or less the same over the past 20-30 years (Stryker, Boston Scientific, Medtronics, etc.) while the global top pharma companies have changed names or merged - In 1990, the top pharma companies include Bristol-Myers Squibb, Glaxo, SmithKline, Ciba-Geigy while the likes of J&J, Pfizer, Roche were then only second tier (10-15 largest). In 2000, Pfizer and AstraZeneca jumped to top 5 (together with a merged GSK), and fast-forward to today, none of the top 5 names back in 1990 was still standing.

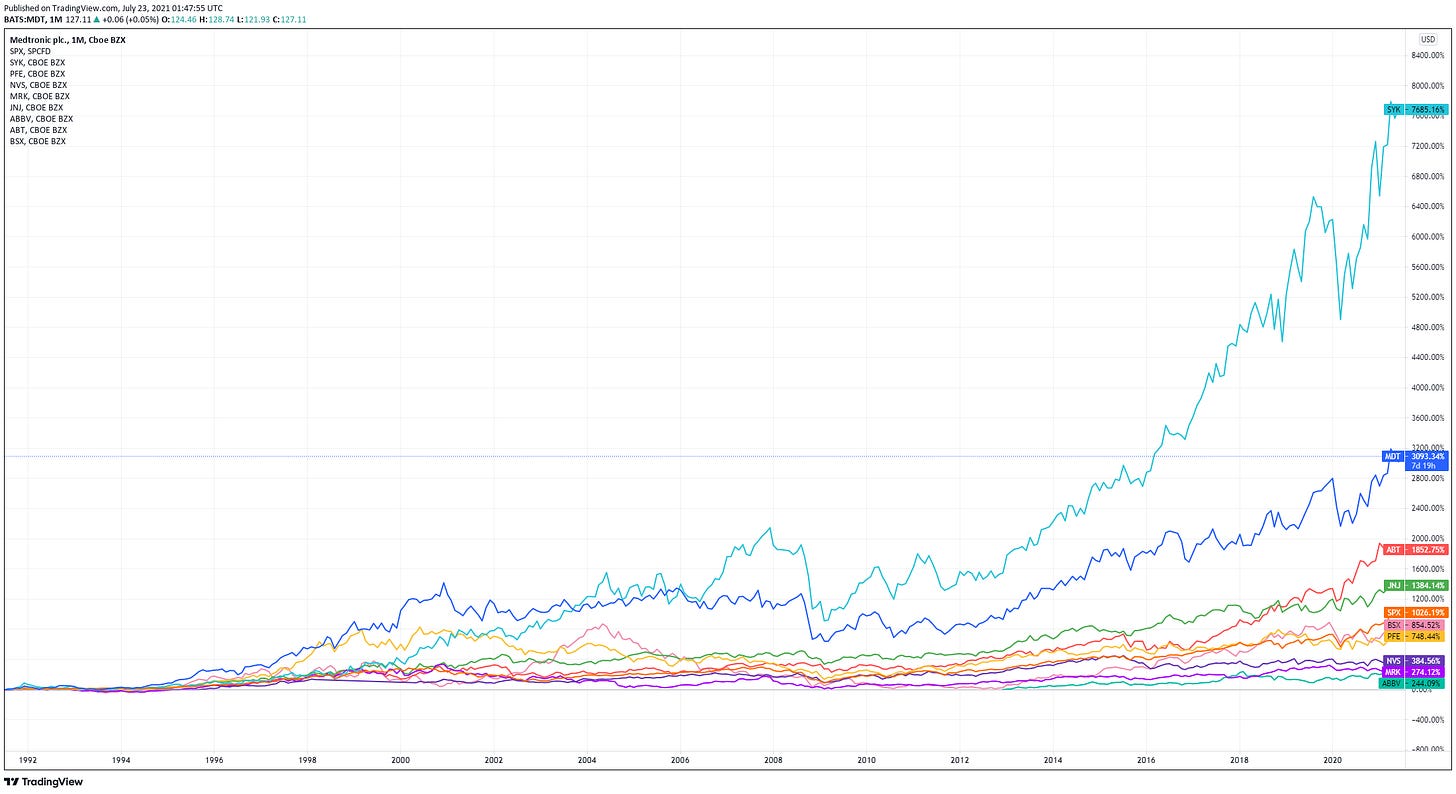

The share price performance in the past 30 years of the largest Medtech companies outperformed by a large margin vs. the largest pharma companies and the S&P 500 index. (the top 4 lines are Stryker, Medtronic, Abbott and J&J). Interestingly, the big pharmas actually just about underperformed the S&P 500 index for the past 30 years or since they were listed!

The above two observations beg an explanation that I feel highlight one of the key structural difference between the two industries. In pharma, the process of drug discovery can be random, serendipitous and success is not guaranteed or directly correlated with amount of R&D spending. Furthermore, once a new drug has been discovered, the patent usually lasts for 20 years, during which the company needs to constantly pour large sums of R&D money, in the hope of stumbling upon the next big discovery.

If we look at the history of Abbvie, the success of a single blockbuster drug Humira can really drive the success of the entire company. Consider this: Abbott Lab (before Abbvie was spun out) bought Knoll Pharma in 2000 for $6.9bn and got the patent to Humira. Humira’s growth is staggering due to its ability to keep expanding indications to treat numerous different conditions (like a Swiss-Army knife). In the first full year of sales, Humira generated $280mn and it grew at a CAGR of 28% for 17 years(!), and in 2020 generated almost $20bn in sales, accounting for 50-60% of the total sales in Abbvie. A purchase price of $6.9bn for a lifetime revenue of $173bn and counting (What a deal for Abbvie!)

At Merck, the fascinating story of how the blockbuster oncology drug Keytruda rose like a pheonix from the ‘dumped’ pile of research pipelines to ultimately generating >$14bn in annual sales and accounting for 1/3 of Merck’s total pharma sales. What is more fascinating is that the drug was initially discovered in a Dutch company called Organon, and was totally not intended to treat cancer. In fact, the team set out to find drugs that would stimulate PD-1 protein to treat autoimmune diseases but ended up in the opposite direction of inhibiting PD-1. The research program went through two M&As before ended in Merck which designated it low priority and ready to sell away the program for close to nothing.

I will not be surprised that such stories abound in the drug discovery world, which ultimately means that drug discovery is not a linear process and hence it is entirely possible to see episodes of David defeating Goliath if a small biotech firm stumble upon a superdrug that drastically altered the competitive landscape. The long term success or failure of companies rest on the constant serendipitous discovery of the next novel blockbuster drug.

On the other hand, the medical device industry is a multi-disciplinary one that requires a combination of expertise from biochemistry, material science, precision engineering, fluid dynamics, etc. The R&D and improvement process is much more cumulative with new product launches relying on the foundations of earlier R&D work. As such, medical device discoveries generally progress linearly or in step-function. For example, many medical implants often started out as a 1st generation device and then subsequently launched a 2nd or 3rd generation products with better efficacy or clinical outcome. Furthermore, unlike drugs where it is either injected or swallowed, medical device companies have to consider ease of use and functionalities, and have inherent stickiness with the doctors once they get used to a certain brand and product features. As such, it is harder for competitors to ‘copy’ a medical device given the various moving parts and cumulative technical know-how in years of R&D and engineering (unlike in the pharma generics space where anyone can make the same drug once the patent protection is over). All these mean that each R&D dollar spent will ultimately translates to a stronger IP or sales for a medical device company vs. a pharma company, and such differences get compounded over time. In other words, medical device companies are able to constantly dug out a larger and deeper moat as they build up IPs and technical know-hows, which explains why the giants can remain giants for a long time in medical device industry.

4. 骨科3D打印逼近国际水平,突显研发能力

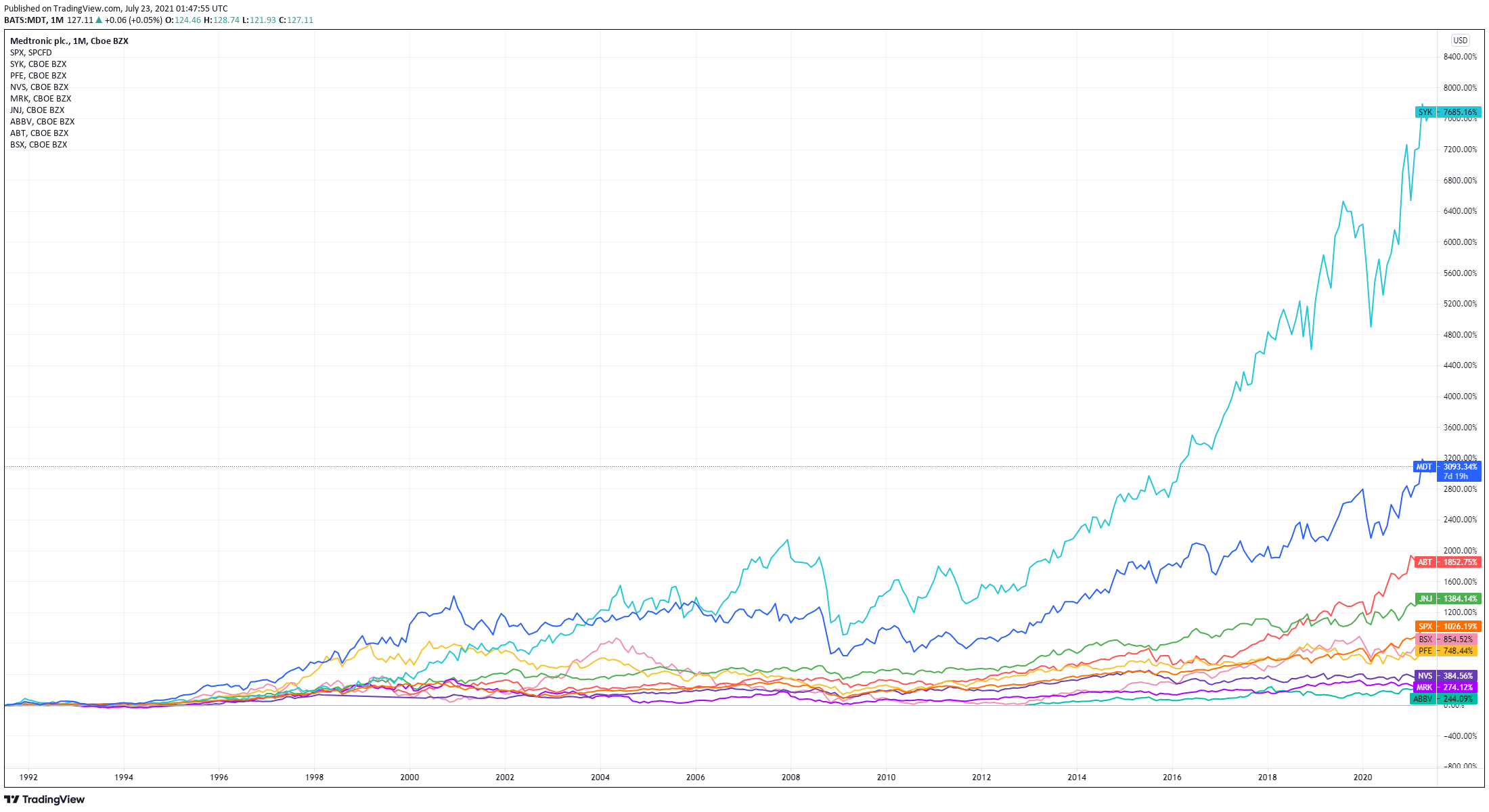

AK Medical has invested heavily in R&D over the years, and spends a larger % of sales on R&D relative to both domestic and global peers. This has resulted in higher number of patents across the orthopaedic portfolio, particularly so in the 3D printed field (note: Weigao and Double Medical have higher number of Class II devices due to their focus in trauma and spinal products)

AK Medical’s leading position in 3D printed orthopaedic implants is the key differentiator among the domestic peers, which I believe demonstrates its forward-looking vision and strong in-house R&D team. In 2015, AK became the first company in China to get approval on a commercial 3D-printed product, and in 2020 has in total 5 approved 3D-printed products - 3 standardized products in hip implants, artificial vertebral bodies and interbody cages, and 2 customized products in pelvis implants and cervical fusion. Though still behind the global powerhouses such as Stryker, I believe AK’s advances in 3D printed implants are catching up fast. From 2016-2019, 3D printed sales have grown at CAGR of 120%, and was flat in 2020 (123mn to 126mn) due to Covid-19. Margins for 3D printed products are higher and are outside the scope of the centralized procurement, given its niche and innovative nature. Government has in fact published clinical guidelines to encourage surgeons’ adoption of 3D printed products. This is a space to be closely watched once Covid and centralized procurement have settled down.

A key catalyst for adoption of 3D printed implants is a 3D surgical platform for surgeons to simulate and plan their surgeries, with inputs from a 3D clinical data. AK Medical, being the forerunner in 3D printed implants, has a proprietary platform called 3D ACT which helps lower the barrier of adoption for surgeons - from converting CT/MRI imaging to 3D models, to selecting customized or off-the-shelf implants and personalized instruments. I believe that as the cost of offering such personalized implants drop, more surgeons and patients (especially for revision or tumour cases where the surgery is more complicated to perform) will adopt it. It’s amazing to think that in dental braces we customized each brace to an individual’s teeth and mouth shape (and even colour preferences), while currently we shave off healthy bones and cartilages to fit standardized implant sizes.

Another key differentiation for AK Medical is its greater market share among domestic peers in both the knee replacement sub-specialty and the revision surgery market, both of which have higher technical barriers and currently still dominated by global firms. Knee replacement is currently severely under-penetrated in China and I expect it to outgrown the overall joint replacement market, hence placing AK at a much favourable position than the other domestic peers.

5. 骨科集采的未知与利弊,追根究底是概率问题

Volume-based centralized procurement (‘集采’ or ‘Jicai’) is one of the key pillars in CCP’s healthcare reform policy. Essentially, Jicai is a government-led (national, provincial or city-level) group-buy policy that guarantees the tender winners a specified minimum volume in exchange for price cuts. This procurement policy is not something new and have been experimented and tested in various ways, and applied nationally to generic drugs back in 2017/18, and lately to coronary heart stents in 2020.

Regarding the question of what medical devices/consumables could be subject to Jicai, various government officials have clarified their stance, and that there are a few key criteria before central or provincial governments will consider applying Jicai:

High clinical usage volume

High total reimbursement value

Relatively mature and clinical-proven medical implants/consumables

Medical implants/consumables with relatively strong competitive landscape

Relatively undifferentiated products with comparative clinical outcomes

With the above criteria in mind, it is understandable that orthopaedic products will fall into the ‘chopping board’ of the authorities. However, investors have to bear in mind what exactly is in scope for the Jicai, and how much does AK Medical’s sales fall under the blade. 3D-printed products (except for standardized metal 3D printed hip joint implants), revision surgery products, overseas sale, which collectively accounts for an estimated ~30% of total sales, will not be subjected to Jicai.

To fully appreciate why the CCP is taking such a drastic regulatory measures and understand their rationale, it will probably require a much deeper understanding of China’s healthcare system and the factors driving its development to date - political culture, economic history and societal norms. It is an fascinating discussion and I am still constantly learning about this, but will not elaborate it here (may require a full PhD thesis to lay out all the thoughts). Suffice to say, the core objective of the CCP is to lower costs for patients while reducing financial burden on the National Healthcare Security, and to achieve this by cutting middemen, reducing kick-backs and diluting purchasing powers from hospitals/doctors. To give two jaw-dropping examples,

A core hip implant component cost of production can be RMB900, ex-factory price increase to RMB3,000 (GP margin of 70%) and after a few layers of ‘distribution’, the final price that a patient pays can increase to RMB 25,000.

A drug-eluting stent (DES) costs about RMB 14,000 in China, while the same costs RMB 2,500 in Brazil, RMB 2,600 in India (capped), RMB 6,880 in France, RMB 8,000 in the UK, RMB 12,000 in US and Japan.

The above really begs the question of where did all the profit margins go, and also proves that manufacturers can probably earn a decent profit margin with a much lower end-user price.

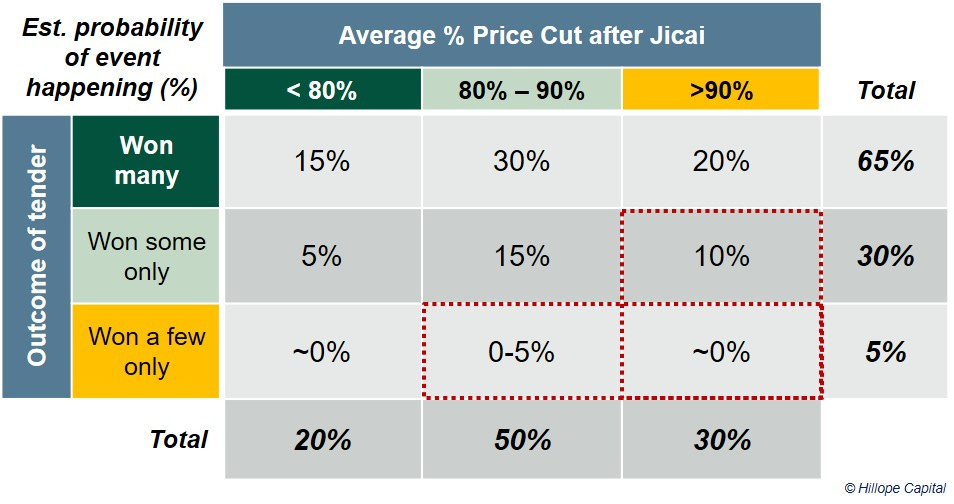

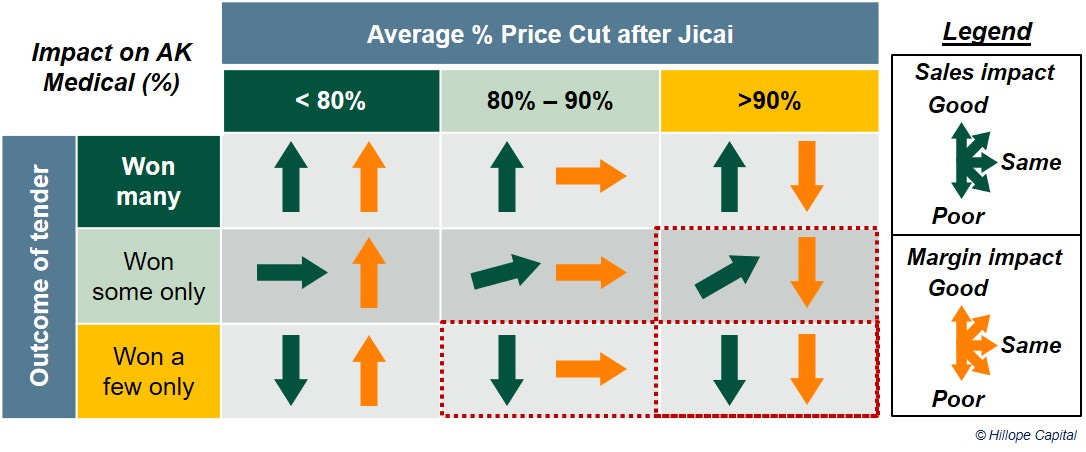

The impact or uncertainty of Jicai on firms ultimately depends on two unknowns - % price cut and whether a company wins the tender (and how much volume vs. pre-Jicai). To understand the impact, it is useful to consider a 3x3 probability matrix and tackle each scenarios one by one, focusing on the downside cases. Investing, at the core, is trying to understand as accurately as possible the future probability cone and striking when the odds are in our favour.

The above are my best estimation of the likelihood of the various scenarios happening in Jicai, and what the impacts are on sales and margin. I think the impact of various scenarios on margins can be estimated with a fair degree of accuracy, but what the market is pricing in right now is the risk that price cuts are extreme (>90% as evident from the recent coronary stent national Jicai), and the uncertainty around whether a company (in my case AK Medical) will win the tender. Let’s tackle them one by one:

On the likelihood of extreme price cut, it is worth noting that only in cases where price cuts are >90% will margins start to meaningfully deteriorate. This is not only because manufacturers have quite significant pricing room to absorb cuts but they can also shift their operation model to reduce distributors, opt for direct sales, outsource to contract service organisations, etc. such that there will be savings from SG&A which will partly mitigate GP margin decline due to ASP decline.

Markets have generally priced in a >90% price cut due to the policy pressure from the highest level (and the fact that many local gov’t officials often try to implement a harsher interpretation of the state regulations to earn political ‘points’), and the precedent from the coronary stent Jicai was a slap in the face for many who still believe in a mild regulatory environment. However, there are three key differences between coronary stents (or even trauma) and hip/knee implants - 1) GP margins for stents or trauma products are higher to begin with (~80-90%) and the production process is less technically demanding, 2) domestic market share of stents is ~80% with import substitution largely taken place and pricing difference between imported and domestic stents are relatively small, and 3) coronary stents have less product differentiation. Hence, in such a relatively mature and competitive market, companies are forced to choose the lesser evil which is to go all out and bid for huge price cuts in order to capture market share. However, in the case of hip/knee implants, imported brands can costs 2-4x more than domestic brands and there are difference materials used in each implant system (metal, PE, ceramics, etc.) with higher technical know-how in terms of production, and I believe that such a competitive landscape will lead to a higher price floor and less fierce price-cutting battle.

On the likelihood of AK Medical winning tenders, this is a risk that carries catastrophic consequences if it ever materializes (just take a look at Sinomed SH:688108 and its impact after falling out of the stent Jicai). This is also largely why the market participants (renowned for hating uncertainties) run for the emergency exit and watch how the ‘fire’ will play out first. To me, if we believe that the government ‘favours’ domestic firms, it is very unlikely that AK Medical, being the current leader in terms of volumes of implants sold, will not win most tenders. In fact, compared to coronary stents where there isn’t much market share to steal from imported brands, Jicai in hip/knee implants will be the real deal in driving the import substitution trend as mentioned above. Coupled with AK Medical’s strong R&D capability, quality products and KOLs/hospital networks, it is very unlikely that it won’t win a higher volume than before.

On the question of whether domestic brands will suffer market share after price cuts. Consider this scenario - a RMB 60,000 imported implant vs. a RMB 25,000 domestic (a 35,000 difference) will become RMB 12,000 and RMB 5,000 (only 7,000 difference) after a 80% price cut. Will patients insist on getting the imported one since these things stay in their body for 10-15 years? It is a difficult question to answer but I believe the answer is not really. The arguments are: 1) Jicai dictates the volume for each brand that won the tender and hospitals have to fulfill the volume first, 2) based on historical usage, AK medical already has the largest implant share in terms of volume (~15% volume share but only ~7-8% in sales share) and won the trust of many doctors/patients, 3) reimbursement rate % still differs between domestic vs. imported brands, hence the above number becomes more like RMB 6,600 and RMB 1,500 out-of-pocket (difference is now optically more meaningful), 4) with a similar pricing dynamics, coronary heart stents and trauma implants are dominated by domestic products already, 5) quality of domestic products are shown to be close to, if not on par, with imported brands (quality difference doesn’t justify pricing difference).

Indeed, the recent rules announced on 21 June on hip/knee implant Jicai corroborated some of the above hypotheses. A few key points to note:

Product groupings and the concept of ‘一品一策’: hip implants are divided into metal alloy-metal-alloy, PE-ceramic and ceramic-ceramic

A/B Grouping to differentiate quality of manufacturers, which means less competition for those that managed to enter Group A (that will consists of the existing import brands), which AK Medical has a high chance of entering

Larger than expected number can win the tenders (not like in many previous Jicai where many firms fight for a limited number of seats)

Pricing includes the overall service delivery including instrumentation and accessories, transportation, ancillary services such as sanitization, etc. - this shows government’s thoughful policy-making and also illustrates the key challenges between a drug Jicai and medical implants Jicai

Price is not the only determinant - this to me is the most critical shift in regulators’ mindset (possibly due to lessons learnt from the drastic price cuts in stents)

The above really demonstrates that the goverment is experimenting and tweaking their policies as they go, recognising the nuances involved in high-value medical implants, and the importance of supply and quality in addition to price alone.

In summary, one of my key insight into AK Medical is that the probability of AK Medical being hit significantly by Jicai is low while the market has priced in a much higher than expected probability. I am eagerly waiting for the Jicai results which is expected to be annouce in Sep 2021.

6. 带领管理团队的创始人是骨科外科医生起家

Founder of AK Medical is a man called Li Zhijiang (李志疆), who owns 46% of the company. LZJ appears to be a very low-key person with very little written or made public about him online. Before starting AK back in 2003, he worked as a Marketing Director for 2 years at another orthopaedic firm (北京天义福医疗器械有限公司) in Beijing, gaining experiences in sales and marketing. Prior to that, he worked at Stryker China from 1999-2001 as a Product Manager. Prior to that, he spent 11 years from 1988-1999 as a orthopaedic surgeon at 河北省唐山首钢矿山医院. LZJ once said in an interview that the best medical device product is always the result of the combination of clinical driven needs with superb product engineering. Indeed, if we look at the founders of leading global MedTech companies, they are mostly founded by physicians (Stryker, Abbott, Baxter, Intuitive Surgical). I believe that there is an edge in surgeon-founded MedTech companies due to better product development capability and clinically-driven R&D. The unique characteristic of medical devices is that though patients are ultimate end-users, in some sense doctors/surgeons actually are the key decision makers in terms of purchasing decisions and play a huge role in identifying clinical gaps and patient needs.

7. 国际视野与并购能力体现长远目光

Since listed in Jan 2018, AK Medical has stuck to its IPO plans of doing strategic M&A acquisitions. AK has acquired JRI in Apr 2018, a UK-based orthopaedic implants company founded >50 years ago, and Beijing Libeier in Apr 2020 from Medtronics China. I believe both acquisitions were the right strategic move by AK - JRI helping to acquire expertise in orthobiologics, shoulder implants and a platform for overseas expansion; while Libeier fills significant gaps in AK’s current orthopaedic portfolio (spine and trauma). Both acquisitions demonstrate management’s vision to be a diversified global player in orthopaedics, and I think both were done at reasonable prices (27x P/E for Libeier, JRI was loss-making and 1.5x P/B). Many companies fail at acquisitions or do it for the wrong reasons but I believe AK has proven its ability to deploy capital at value-accretive acquisitions (After consolidating JRI, sales grew from RMB 69m in 2018, to RMB 92m in 2019 while operating profits grew from RMB 230k to RMB 13.7m, though results fell in 2020 due to Covid.)

Great work!